Thinking About Growing a BaaS

What is a BaaS?

Banking as a Service (BaaS) provide access to deposit accounts and methods to move funds in & out of those accounts. They tie together pieces of the FinTech delivery stack to enable third parties to develop thin client applications. The BaaS often provides user facing applications that can be white labeled (e.g.; mobile apps, consumer websites, support portals, etc.) for third parties to use to accelerate go-to-market distribution.

The most simple of BaaS providers usually enable:

- Opening of deposit accounts

- Debit card issuance

- ACH services

- Compliance services for all of the above

With just the above, third party developers can build challenger banks, lending products, insurance & claim disbursement systems, expense management tools, services for the gig economy, and plenty more.

How do BaaS Make Money?

BaaS providers earn money in several ways:

- Licensing fees/Transaction fees: A toll for access to the infrastructure. This can be charged akin to SaaS platforms with a monthly fee for “all you can eat” transaction volume or on a per transaction basis.

- Professional servicing fees: Markup of human services, often for technical configuration, servicing or compliance time.

- Float: Yield on deposits shared by the banks and sourced from banks’ ability to lend against the deposits.

- Interchange: Yield on transaction volume, which will differ by transaction type. Sometimes these are sources by the payor (remittance margins) and sometimes the payee (card IX).

At the end of the day, BaaS models are both directly and indirectly dependent on the latter two. The BaaS model uses FinTechs (and the developers who build them) as lever points to drive deposit and transaction volume through their ecosystems to generate yields. Instead of acquiring the end users — whether consumers of businesses — who will provide the deposit and transaction volume, BaaS providers let others build applications and pay for the acquisition of deposits and transactions. And at the end of the day, either or both the BaaS and FinTech generate their margin from yields from float or interchange (or lending).

Understanding the above, makes it clear what a BaaS objective must be from a product perspective: Provide an offering that makes it as easy as possible for third parties to launch FinTechs that drive deposit and transaction volume.

Understanding How BaaS Connect Payments Infrastructure for FinTechs

BaaS providers are bundlers who piece together the financial infrastructure such that it is easier for FinTechs to offer services from all of technical delivery, contractual, and startup capital perspectives. Simply put, the bundling enables two things:

- Opening of accounts

- Moving money in and out of those accounts

A limited offering will have a sponsor bank, connect to the card networks through a processor, and will either directly or through a processor tap into other networks to facilitate additional ways of moving money.

BaaS providers can expand to offer compliance services and additional transaction types leveraging the payment rails in their core offering. For example, “Early ACH” is popular feature of several challenger banks. The execution of this feature is the same:

- Issuer receives an ACH file with an effective date in the near future

- The file is parsed to determine who is receiving funds and from whom

- When an incoming ACH is considered low risk, the issuer enables a value load to the payee knowing that good funds will settle two days later.

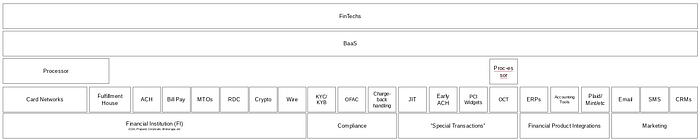

There are several other transactions or flows that are of high value that BaaS providers can offer, with just a few shown below.

Beyond the pure financial offering, there are integrations that BaaS providers can offer to help their FinTech customers decrease CAC and churn.

- Financial Product Integrations: Easy connections to Plaid so transactions and accounts can be monitored on third party apps or connections to accounting tools & ERP systems to streamline corporate financial operations.

- Marketing: Integrations into CRMs, SMS tools, and email systems for marketing and transactional notifications

- Marketplace: Offering a bundle of non-financial products to cross-sell into customer bases to drive incremental revenue

At some point the BaaS bundles the right permutation to produce an offering that FinTechs think they can use to deliver their applications.

Other Considerations: Removing Friction, Too Many Hands in the Cookie Jar & Compressing Margins from Vendors & Customers

Once a delivery stack is put in place, BaaS providers have to solve (at least) three problems:

- How to remove friction to catalyze transaction volume?

- With so many hands in the cookie jar trying to share yield, how does a BaaS ensure their offering drives enough margin?

- Once programs scale, how do BaaS providers make sure their vendors and customers do not aggressively eat into margin to turn unit economics upside down?

To make matters more complicated, a BaaS provider has to ensure their vendors and customers are satisfied with their economics. Without vendors, it is impossible to offer services and switching costs are generally high. Without customers, there is no deposit or transaction volume and – while their switching costs are often high – FinTechs will do so if they achieve requisite volumes and can afford the large upfront expense in order to drive their own longer term margins and cash flows.

Driving Growth: Vertical & Horizontal Expansion

To drive growth, the considerations become:

- Do you drive volumes by horizontally expanding?

- Or do you drive margin by vertically expanding?

Thinking About Horizontal Expansion

Horizontal expansion helps to define product-market fit. At some point, a BaaS reaches the right permutation of bundled services to acquire programs who can in turn acquire customers. The core services mentioned at the top of this post are generally enough to get going, but won’t often lead to any differentiation. They are table stakes.

The quandary for a BaaS provider is when, if ever, the permutation of transaction and account types becomes a true differentiator. The FinTech delivery stack is commoditized. Differentiation comes on two fronts:

- Removing friction for FinTechs to access the tools and use whichever permutation they need in order to launch their applications. Catalysts to achieving this include choosing the right vendors & executing on product delivery.

- Pricing.

There are straightforward and creative ways to achieving both.

Thinking About Vertical Expansion

Vertical expansion helps expand unit economic margin, but will bring CapEx and OPEX requirements. At the right volumes, this is an easy trade to make if a BaaS has access to capital.

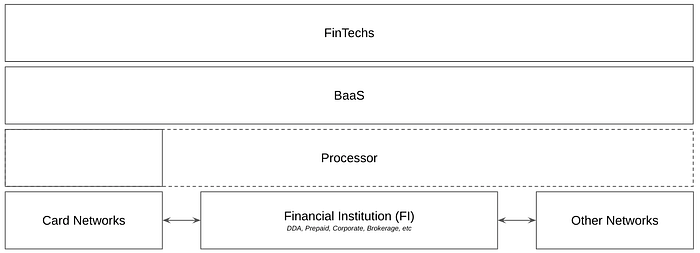

Below is a simplified illustration of a FinTech delivery stack.

Vertical integration usually starts with the non-card networks. Instead of relying on a processing partner to connect to bill pay, money transfer, ACH networks and others, the BaaS can hook directly to them. The BaaS still will leverage other transaction types connected to their FI’s core, but in doing so will change the margin profile of transaction for the positive.

BaaS providers can do this until they decide to become a processor themselves. Companies like Marqeta and QRails have invested in the requisite security to directly connect into the card networks, enabling even more margin expansion. SoFi went so far as to purchase their processing partner, Galileo.

Being able to offer pure processing and program management (i.e., Baas) services affords a BaaS provider the flexibility to allow their customers to grow with them, to change pricing model at different levels of scale, and to change who owns the liability on compliance issues. As discussed above, this means that customers who provide large volumes can transfer to a pure processing relationship which, although it will bring lesser margins, does enable the BaaS to keep the volumes.

BaaS providers can also try to become their own bank. While every VC pitch includes a future state of “we will become a bank,” very few actually have. It is costly, introduces new risk, and dramatically changes operations. But it is not impossible! Green Dot issues its cards and offers its banking as a service through its own bank. While the overhead is larger, they also control their own destiny to offer products that adhere to the letter of the law as opposed to introducing additional constraints for fear of not even coming close to approaching regulations.

The card networks are very entrenched. BaaS providers will not be able to replace them. They can, however, flank them though to expect to do so broadly would be an expensive proposition. By providing wallets to merchants and offering the front-end of the acquiring side of the payments stack, BaaS providers can route transactions around the card networks facilitating what is, in essence, the equivalent of a p2p transaction (with just one “p” being a business). When you see Venmo offering merchant accounts that can “venmo,” this is exactly what they are offering.

Replicating Globally

At any point a BaaS can decide to enter a new market. This means a full or partial replication if the delivery stack. BaaS providers can offer tremendous value to FinTechs by normalizing the data sent and received by API endpoints, while routing transactions to through the appropriate partners on the back end. Doing so let’s FinTechs build once for multiple markets and creates additional stickiness such that it is harder for them to leave their BaaS provider.

Further, in markets where it is easier to obtain and maintain certain licenses, a BaaS provider can offer a more vertically integrated offering in one geography versus another.

Timelines, Capital Requirements, and Priorities

While it’s nice to outline a path to world domination in a blog post, in reality everything discussed here would cost tens of millions of dollars and take years to accomplish.

So how to prioritize?

Well, in short, it depends. Questions BaaS providers should be asking themselves include:

- How much incremental volume would adding a new transaction type yield?

- How much margin expansion comes from owning more of the delivery of a transaction a BaaS provider already offers?

- Can I replicate my delivery of a permutation of transactions in another geography? And, if so, what’s the size of the market and economics in that market?

All of these questions attempt to answer the question of what is the fast way to generate incremental gross margin, especially in consideration of the capital requirements and the BaaS’s cash position.